From the United States Treasury Department:

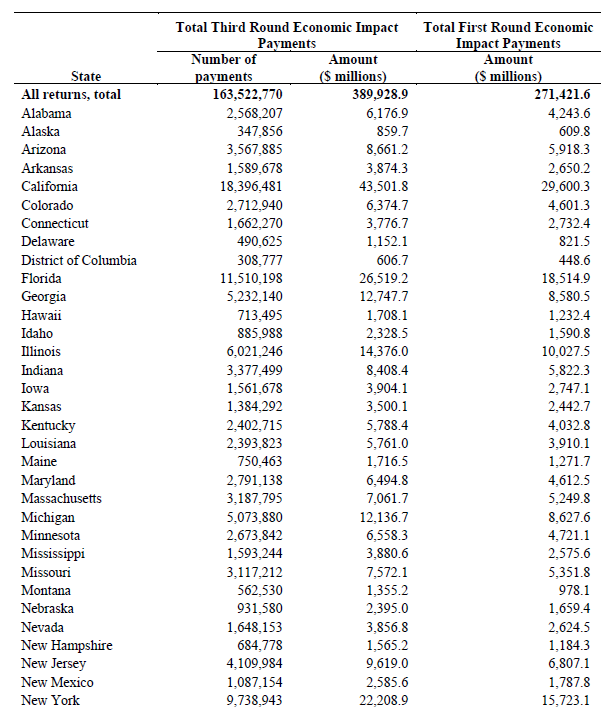

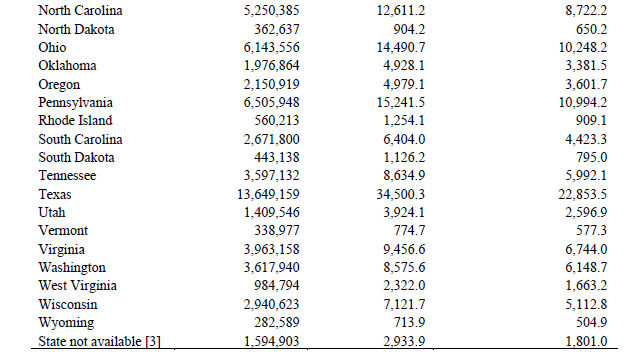

Recently , the U.S. Department of the Treasury and the Internal Revenue Service (IRS) released state-by-state data through early-June for the 163.5 million Economic Impact Payments (EIPs) totaling nearly $390 billion received by individuals through the American Rescue Plan Act. With this round of payments, the IRS and the Bureau of the Fiscal Service (BFS) have delivered more EIPs and more total direct relief than in any previous round of direct relief. All 50 states saw more total relief with this round of payments than in previous rounds.

The EIP data, available on IRS.gov, cover payments made through June 3 and provide, by state, income category, and filing status, information on the number and dollar amounts of payments, as well as aspects of the payments. More than half of this direct relief has gone to households making less than $50,000 a year. Another 10 percent of the payments went to Social Security, Railroad Retirement Board, and Department of Veterans Affairs beneficiaries whose incomes were not large enough to be required to file an income tax return and to individuals who used the online Non-filer tool. In total, more than 85 percent of the payments went to households making less than $100,000 a year.

The EIPs under the American Rescue Plan included payments of up to $1,400 per qualifying dependent, a significant increase over the $500 and $600 per qualifying child from the first and second rounds of payments, respectively. Through June 3, families received more than $108 billion in Economic Impact Payments attributable to their qualifying dependents under the American Rescue Plan, an increase of more than $78 billion over the first round of EIPs last year.

The IRS and BFS collaborated to deliver the third round of EIPs rapidly, securely, and conveniently to American families. The week after the American Rescue Plan passed, the IRS disbursed roughly 90 million relief payments. Through early June, nearly 138 million households received EIPs through direct deposit, more than during any other round of payments. More than 85 percent of the third round of EIP dollars were paid through direct deposit, up from 77 percent from the first round of EIPs last year.

Additional Information on Economic Impact Payments in the American Rescue Plan Act

Americans eligible for Economic Impact Payments provided in the American Rescue Plan can still receive their payments by filing a 2020 income tax return or, if their income is not high enough to be required to file a full income tax return, by using the IRS Non-filer tool available here. Individuals do not need to have children to sign up for Economic Impact Payments. By filing a 2020 income tax return or using the Non-filer tool, eligible individuals can also claim the 2020 Recovery Rebate Credit for any amount of the first two rounds of Economic Impact Payments they may have missed and to register for monthly Advance Child Tax Credit payments.

The IRS will continue to make Economic Impact Payments on a weekly basis. Ongoing payments will be sent to eligible individuals for whom the IRS previously did not have information to issue a payment but who recently filed an income tax return, as well to people who qualify for “plus-up” payments.

Under the American Rescue Plan, eligible people filing as single making less than $75,000, a head of household making less than $112,500, or as married couple filing jointly making less than $150,000 qualify for an Economic Impact Payment of $1,400 per person each plus $1,400 for each qualifying dependent, including kids, college students, and seniors claimed as dependents. An eligible married couple that earned $75,000 last year and had two qualifying children would receive an Economic Impact Payment of $5,600 through the American Rescue Plan.

Individuals can check the Get My Payment tool on IRS.gov to see the payment status of these payments. Additional information on Economic Impact Payments is available on IRS.gov.

| [1] Section 2201(a) of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), Public Law 116-136, 134 Stat. 281 (March 27, 2020) added section 6428 to the Internal Revenue Code (Code). Section 6428(a) provides an eligible individual for their first taxable year beginning in 2020 a refundable tax credit of up to $1,200 ($2,400 for eligible individuals filing a joint tax return), plus $500 per qualifying child of the eligible individual. This tax credit is referred to in section 6428 as a “2020 recovery rebate for individuals.” Section 6428(f)(3)(A) instructs the Secretary of the Treasury to make advance refunds of this credit “as rapidly as possible” and before January 1, 2021. The IRS refers to the advance refund of this credit as an economic impact payment Economic Impact Payment (EIP). EIPs made under section 6428 are referred to as a “First Round EIP.” The credit phases out at a rate of 5% of the taxpayer’s adjusted gross income (AGI) in excess of a threshold. The threshold is $150,000 in the case of a joint return, $112,500 in the case of a head of household, and $75,000 otherwise. Those ineligible for the credit are (1) nonresident alien individuals, (2) individuals who can be claimed as a dependent by another taxpayer, and (3) an estate or trust. When spouses file jointly, both spouses must have a valid social security number (SSN) to receive the credit, unless either spouse is a member of the U.S. Armed Forces at any time during the taxable year. In that case, only one spouse needs to have a valid SSN. Eligibility for, and the amount of, a First Round EIP was based on an individual’s Tax Year 2019 return, or if a Tax Year 2019 return was not filed, the individual’s Tax Year 2018 return. Eligible individuals who otherwise did not have a tax filing obligation but received Social Security benefits, Railroad Retirement benefits, compensation and pension benefit payments from the Veterans Administration, or Supplemental Security Income received a First Round EIP without having to file a return. Other eligible individuals who otherwise did not have a tax filing obligation needed to submit information through the “Non-filers: Enter Your Information Here” online portal, or through other special or simplified procedures provided by the IRS, to receive a First Round EIP. Eligible individuals who did not receive some or all of the recovery rebate credit to which they are entitled as a First Round EIP may claim the remaining amount of the recovery rebate credit when filing their 2020 tax returns. The Coronavirus Response and Relief Supplemental Appropriations Act, 2021, enacted as Division M of the Consolidated Appropriations Act, 2021, Public Law 116-260, 134 Stat. 1182 (December 27, 2020) added section 6428A to the Code. This legislation created an “additional 2020 recovery rebate for individuals.” The IRS refers to the advance refund of this credit as a “Second Round EIP.” This legislation also altered for the “2020 recovery rebate credit” the requirements regarding the inclusion of valid SSN and changed the phase-out threshold for qualifying widows and widowers to be $150,000. These statutory changes did not affect the First Round EIPs, as reported in this table. |

| [2] Section 9601(a) of the American Rescue Plan Act of 2021, Public Law 117-2, 135 Stat. 4 (March 11, 2021), added section 6428B to the Internal Revenue Code (Code). Section 6428B provides an eligible individual for their first taxable year beginning in 2021 a refundable tax credit of up to $1,400 ($2,800 for eligible individuals filing a joint tax return), plus $1,400 per qualifying dependent of the eligible individual(s). This tax credit is referred to in section 6428B as a “2021 recovery rebate to individuals.” Section 6428B(g)(3) instructs the Secretary of the Treasury to make advance refunds of this credit “as rapidly as possible” and by December 31, 2021. (In other words, no advance refund may be disbursed after that date.) The IRS refers to the advance refund of this credit as a “Third Round EIP.” The 2021 credit is reduced proportionally as a taxpayer’s adjusted gross income (AGI) exceeds a threshold and rises to a full phase-out amount. The threshold and full phase-out amounts are $150,000 and $160,000 in the case of a joint return or qualifying widow or widower, $112,500 and $120,000 in the case of a head of household, and $75,000 and $80,000 otherwise. Those ineligible for the credit are (1) nonresident alien individuals, (2) individuals who can be claimed as a dependent by another taxpayer, and (3) an estate or trust. When spouses file jointly, each spouse must have a valid social security number (SSN) to receive the individual portion of the credit for that spouse (in other words, for the married couple to receive the full $2,800), unless either spouse is a member of the U.S. Armed Forces at any time during the taxable year. In that case, only one spouse needs to have a valid SSN. An individual without a valid SSN can still receive up to $1,400 for a qualified dependent claimed on the individual’s return if the individual meets all other eligibility and income requirements. An individual’s eligibility for and amount of the Third Round EIP was based on the individual’s Tax Year 2020 return. If that return was not filed as of the initial determination date for the individual’s Third Round EIP, the IRS used the individual’s Tax Year 2019 return to make an “initial” Third Round EIP. If an individual filed a Tax Year 2020 return after the initial determination date for the individual’s Third Round EIP and before the additional determination date, and that Tax Year 2020 return indicated that the individual was eligible for a larger credit amount, the IRS disbursed a “plus-up” payment to the individual. This additional amount was equal to the total amount of Third Round EIP to which the individual was entitled, minus the initial amount that the IRS disbursed to that individual. The amounts shown in the table include both initial and plus-up payments issued by the time the data were tabulated. Eligible individuals who did not file a Tax Year 2019 or 2020 return but received Social Security retirement, survivor or disability benefits (SSDI), Railroad Retirement benefits, Supplemental Security Income (SSI), or Veterans Affairs benefits automatically received a Third Round EIP. The IRS also used information provided by individuals who filed in 2020 a Tax Year 2019 return through the “Non-filers: Enter Your Information Here” online portal, or through other special or simplified filing procedures published by the Treasury Department and the IRS in 2020. The Treasury Department and the IRS provided these 2020 filing options to help eligible individuals who did not have a tax filing obligation to receive a First Round EIP provided under section 6428 of the Code, as added by section 2201(a) of the CARES Act, Public Law 116-136, 134 Stat. 281 (March 27, 2020). On June 14, 2021, the Treasury Department and the IRS released a new “Non-filer Sign-up Tool” on IRS.gov to help eligible individuals who had not filed a Tax Year 2020 or 2019 return to file a Tax Year 2020 return and receive, among other tax benefits, Third Round EIPs. This tool is an update of last year’s IRS Non-filers tool. Similarly, the Treasury Department and the IRS published in 2021 for individuals who do not have a tax filing obligation simplified filing procedures that were based on the simplified filing procedures published in 2020 for the First Round EIP. |

| [3] Includes payments made by the IRS to individuals with an address in Puerto Rico but does not include payments made by the Puerto Rico Treasury Department. |

| NOTES: Detail may not add to totals because of rounding. Table does not double-count payments that were issued, reversed, and reissued. (A reissuance could occur, for example, if a bank account that was targeted for an electronic funds transfer was closed at the time the EIP was issued.) Table does not count reversed payments. (A reversal could occur, for example, if a paper check was returned to the IRS as undeliverable mail). First Round EIP data are through the end of Calendar Year 2020. Third Round EIP data are through 2021 Cycle 22 (June 3, 2021). |

| SOURCE: IRS, RAAS, First Round EIP data from January 2021 and Third Round EIP data from June 2021 |

| https://www.irs.gov/statistics/soi-tax-stats-coronavirus-aid-relief-and-economic-security-act-cares-act-statistics |

Featured photo by Alexander Mils from Pexels